Word to the Wise: M&A Snapshot – Crescent Point Energy Corp. Acquires Hammerhead Energy Inc.

November 28, 2023

Each week, XI Technologies scans its unique combination of enhanced industry data to provide trends and insights that have value for professionals doing business in the WCSB. If you’d like to receive our weekly Word to the Wise in your inbox, subscribe here.

Last week we discussed how Directive 88 may be affecting Junior and Micro companies (please find article here). In keeping with the trend of Major and Intermediate deals is the Crescent Point Energy Corporation’s (Crescent Point) purchase of Hammerhead Energy Inc. (Hammerhead). XI’s role is in providing data and software tools that help evaluate and scope for deals long in advance. Today, our M&A snapshot after-the-fact provides insights for your own evaluations that can be done without a data room and/or for finding “one-off deals.”

When assessing this transaction through different lenses using AssetSuite software tools, we see each company’s asset profile, plus the combined entity and gain valuable insight into the transaction beyond announced high-level acquisition highlights.

Deal Metrics

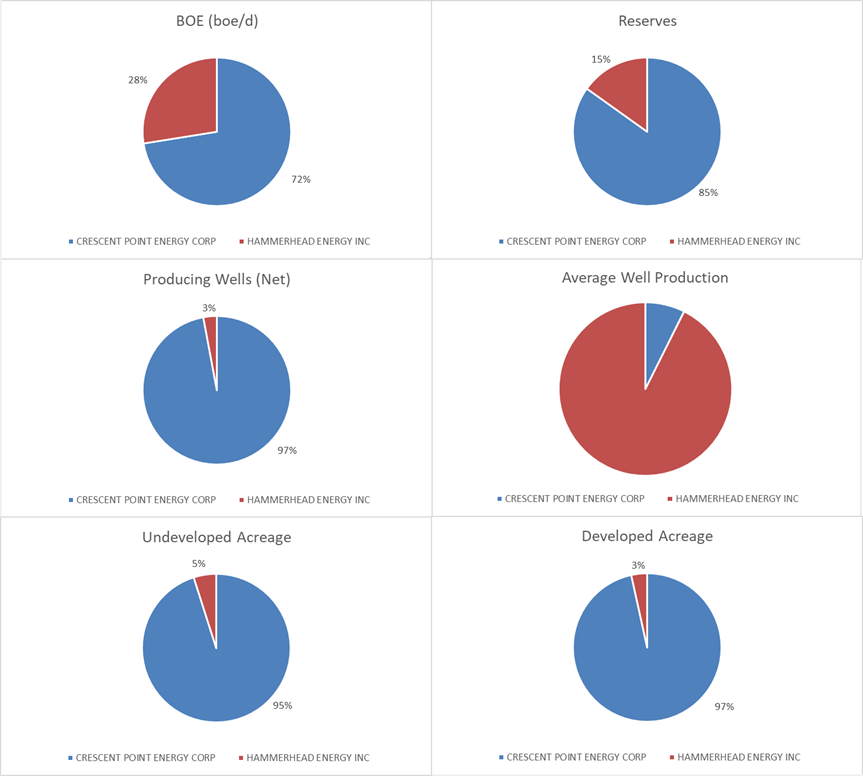

Crescent Point contributes 72% of the production to the combined entity. The companies are relatively similar in terms of operatorship (licensee on file) in that both have a high percentage operatorship, with Crescent Point at 96% and Hammerhead at 99%.

Figure 1 – Working Interest values for Crescent Point (blue) and Hammerhead (red). Source: AssetBook.

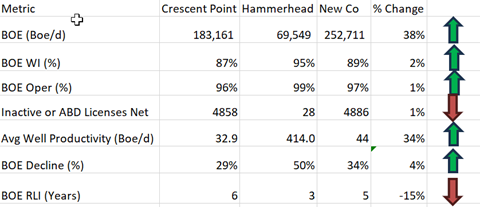

While the absolute numbers tell one story, accretion and dilution metrics tell us more. Looking at the AssetSuite summary, we can calculate some accretion and dilution metrics for this transaction relative to the increase in production.

Per Figure 2 below, this deal is largely accretive. Crescent Point’s production base grew by 38%, operatorship by 1% and working interest by 2%. There is a decrease in the BOE RLI which is to be expected and fits in Crescent Point’s balanced portfolio. These assets are meant to augment their high rate of return but shorter cycle assets in the Montney and Duverney play opposed to their long cycle Saskatchewan assets which will balance out these shorter life assets.

Figure 2: Deal Metrics.

Above numbers are based on three-month average to August production with raw gas numbers at a 6:1 gas to oil conversion. We recognize that Crescent Point’s Kaybob Duverney and Montney plays are likely in the oil phase of development at a different ratio. Source: AssetBook and ARO Manager.

As we can see, the contribution of inactive licenses did have a net negative effect, but very minimal given how accretive these assets are to Crescent Point’s portfolio.

Crescent Point is very spread out over the Western Canadian Sedimentary Basin however, this acquisition augments their recent strategy of moving into the Kaybob Duverney and Montney liquid rich assets that have a very high and quick rate of return. Crescent Point is primarily an oil company and while the AssetBook shows their production as 42% oil based on raw production from the well head, it is again important to note that their Montney assets are in the oil phase of development and therefore this ratio should skew closer to over 50% based on true boe production.

CORE AREA

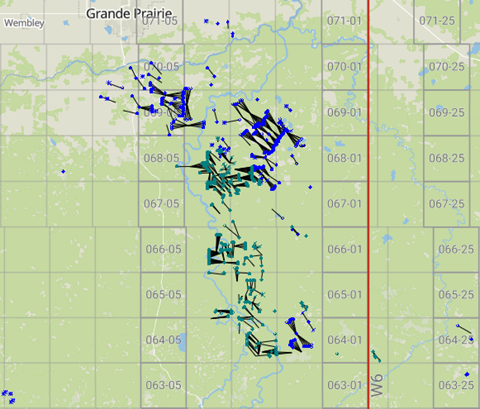

Crescent Point mentions this transaction expands their core operations into their Montney play.

Figure 3 – Map of Crescent Point (Blue) and Hammerhead (Green) Core Area. Source: AssetBook.

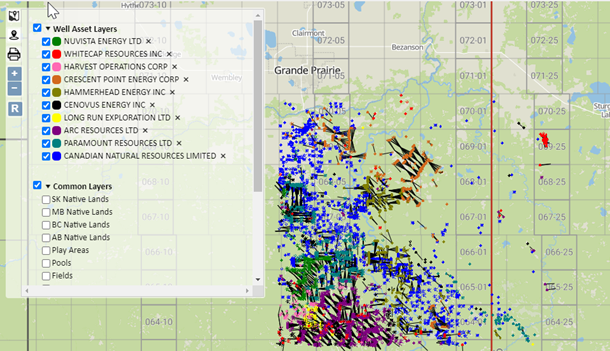

This deal is primarily concentrated in the prolific fields of Elmworth and Karr (as defined by the AER). With the AssetBook we can create an area around these assets to see all other players that may be affected by this deal.

ARC Resources Ltd. (Arc) is the largest player in this area with approximately 108,969 boe/d of production. This area makes up 19% of Arc’s production. Notably, this area makes up 63% of Paramount Resouces Ltd.’s (Paramount) production falling in the top 10 producers of this area with approximately 91,161 boe/d.

There are 31 companies with ten or more boe/day in this area. Download more information on a full list of companies in this area here.

Figure 4 – Top 10 companies in Core Area. Source: AssetBook.

Liability Overview

As the AER is still looking at directive 11 for LCA liability costs and it is important to see the liability cost of the transaction we have used XI’s LLR module to evaluate this. Using an LLR analysis, this deal is slightly accretive to Crescent Point’s LLR ratio increasing it by 2.9. According to AssetBook’s LLR/LCA Module (which only accounts for licensed assets), Crescent Point will absorb $33,708,016 in deemed liabilities, all from Alberta. It’s worth noting that we are not privy to private Site-Specific Liability Assessments, and the deal does involve a number of large-scale facilities, including large scale gathering systems. The majority of the infrastructure is tied in to third party processing plants.

Figure 5 – LLR for Crescent Point, pre- and post-transaction. Source: AssetBook LLR Module.

This figure is slightly higher than XI’s ARO Module working interest calculations which indicates Crescent Point will absorb $33,124,899 in liabilities. As indicated by the very low number of inactive or abandoned liabilities, on a high-level glance, these are very clean assets.

Are there any Emissions Impacts?

While not always discussed as strategic rationale or mentioned in press releases, the emissions impact on the post-transaction entity can have notable implications, particularly form a carbon tax or credit perspective. This deal in particular has minimal overall impact on post-transaction Crescent Point but will bump up their XI-calculated 12-month trailing Scope 1 (fuel, flare, vent) GHG intensity 0.014 to 0.015. The majority of the GHG emissions comes from five Hammerhead facilities that produce ~20k tonnes CO2e or higher. These facilities, as well as a few others, may have TIER-related carbon tax implications.

Figure 6 – Post Transaction Emissions Intensity (Scope 1: Fuel, Flare, Vent; TTM)

While analyzing deals after they are announced is interesting, tools that provide the leg up for looking at your own deals or finding deals proactively to create better value provide a significant advantage. For more results on this acquisition, or to learn more about how XI’s AssetSuite software can analyze potential mergers, acquisitions, and opportunities, including examining potential liabilities and emissions, click here

AssetSuite’s ARO Manager is the only standardized tool for estimating and monitoring asset retirement obligations in Western Canada’s oil and gas sector. To learn how ARO Manager can help with your planning and reporting of liability management, join us for our virtual information session.

Webinar: ARO Manager for Financial Tracking & Reporting.

When: Tuesday, December 5, 2023 @ 9:30am MT

Register here, or visit XI’s website and contact XI for a demo.